One thing that goes along with the current model of hourly-rate billing by law firms is a positive cash conversion cycle. In other words, the time between the work you perform for a client and when you bill them is essentially a 0% interest loan that you’re extending to the client for legal services. In this post, the author explains the cash conversion cycle concept and argues for keeping the time between work and payment by the client to a minimum. What the author doesn’t discuss is why a law firm’s cash conversion cycle should be positive in the first place. Before jumping into that, I want to give a concrete example of what the cash conversion cycle is, and what makes it either positive or negative.

Suppose, for the sake of keeping things simple, that you only have one client and one supplier (maybe Office Depot, who ships all of your paper, pens, and peanut butter pretzels to you). I’m ignoring rent and other expenses, again, just to keep things simple. If you feel like seeing the more detailed equation and explanation, check here.

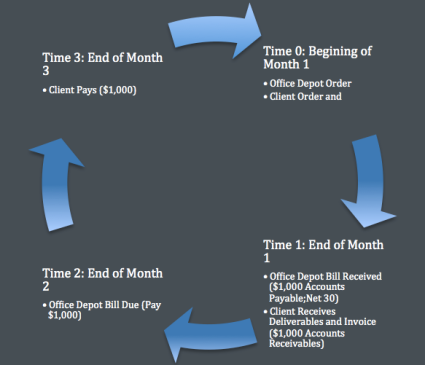

You place an order with Office Depot the beginning of the month, and they bill you on the last day of the month, giving you 30 days to pay the bill. Your bill is $1,000. Now suppose you performed work for your client over the course of that same month, and send them an invoice for $1,000 at the end of the month (It’s a rough hand-to-mouth time for your firm that month…). Now subtract the time you have to pay your supplier from the time it takes to collect receivables, and you have your cash conversion cycle. If you pay Office depot on the 30th day after they bill you, and your client also pays you the 30th day after you invoice them, your cash conversion cycle is 0 days. There is no difference in the amount of time you hold accounts receivable and accounts payable.

You place an order with Office Depot the beginning of the month, and they bill you on the last day of the month, giving you 30 days to pay the bill. Your bill is $1,000. Now suppose you performed work for your client over the course of that same month, and send them an invoice for $1,000 at the end of the month (It’s a rough hand-to-mouth time for your firm that month…). Now subtract the time you have to pay your supplier from the time it takes to collect receivables, and you have your cash conversion cycle. If you pay Office depot on the 30th day after they bill you, and your client also pays you the 30th day after you invoice them, your cash conversion cycle is 0 days. There is no difference in the amount of time you hold accounts receivable and accounts payable.

Now suppose the same situation, but instead your client waits 60 days to pay you. To pay Office Depot on the 30th day after they bill you, you pull $1,000 out of your firms working capital account. You now have a positive cash conversion cycle of 30 days. In other words, you are holding accounts receivable for 30 days longer than accounts payable. For those 30 days you are allowing your client use of the $1,000 while you pay the expenses on behalf of what would otherwise be their funds owed to you.

Now suppose the same situation, but instead your client waits 60 days to pay you. To pay Office Depot on the 30th day after they bill you, you pull $1,000 out of your firms working capital account. You now have a positive cash conversion cycle of 30 days. In other words, you are holding accounts receivable for 30 days longer than accounts payable. For those 30 days you are allowing your client use of the $1,000 while you pay the expenses on behalf of what would otherwise be their funds owed to you.

Now add one more element: your cost of capital. For simplicity, lets assume you’re fully debt financed with a weighted average of 10% interest on the loans you have outstanding (this 100% debt financed firm isn’t realistic, but if we incorporate your equity, we would need to find the expected rate of return on that equity, and then find the WACC, which is more complicated than we need to be here).

In the second scenario you’re using capital that costs you 10% while your client is using that same amount to either earn interest or benefit from in some other way, even if its just greater liquidity. You don’t charge your client interest on the amount they owe you, and instead just eat the cost of capital you for the 30 days difference between accounts receivable and accounts payable.

The article cited first, above, proposes to resolve this by insisting on a larger retainer from clients that take their sweet time in paying your bill, which may bring you to a negative cash conversion cycle on some clients’ accounts. But why not have a negative cash conversion cycle for all clients?

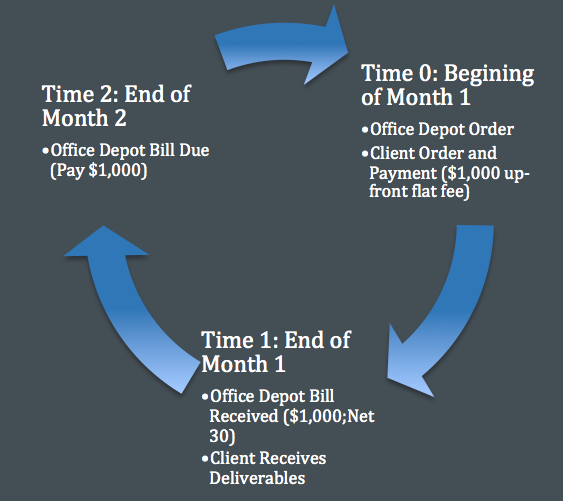

This is one of the perks of charging an up-front flat fee. Not only would your clients appreciate the certainty it gives them in their budgeting, but its something your firm can benefit from in the form of a negative cash conversion cycle. Here’s what it looks like.

At the beginning of the month you place the Office Depot order and collect your$1,000 flat fee. At the end of that month you deliver the work-product to your client and get your bill from Office Depot. As usual, Office Depot gives you 30 days to pay, and you take advantage of that, paying on the 30th day. You have held the $1,000 for 60 days (assuming the first month had 30 days), and you’ve invested it in something that has offset, matched, or exceeded your 10% cost of capital. In other words, interest to you on that $1,000 from the client has either offset, matched, or maybe even exceeded the cost of $1,000 from your lender.

At the beginning of the month you place the Office Depot order and collect your$1,000 flat fee. At the end of that month you deliver the work-product to your client and get your bill from Office Depot. As usual, Office Depot gives you 30 days to pay, and you take advantage of that, paying on the 30th day. You have held the $1,000 for 60 days (assuming the first month had 30 days), and you’ve invested it in something that has offset, matched, or exceeded your 10% cost of capital. In other words, interest to you on that $1,000 from the client has either offset, matched, or maybe even exceeded the cost of $1,000 from your lender.

In addition to the finances discussed above, you’ve reduced your stress because your firm has great liquidity when the expenses come due. You can budget with a high degree of certainty, and know exactly what’s going to happen 60 days after you receive the funds.

Lets suppose you can’t find a short term investment that gets you the rate of return you want (ideally 10% or higher in the case above). Instead of investing it in something new, you pay back $1,000 of your outstanding debt. By taking this rout, you’ve avoided the 10% cost on $1,000 of capital. When the Office Depot bill comes due, use new income or the loan money in your firms working capital account: either way, you just avoided paying $100 in interest to your lender.

The scenario above is possible to put into practice, but your firm needs to be open to using flat-fee arrangements and you need to properly price your services. Pricing can be hard, but it can be worth it. Flexibility in firms may be the more difficult element.

Firms that do make this shift, and can truly leverage it to their advantage by earning rates above their cost of capital, may be able to use those earnings to lower prices or offer a form of rebate, giving them an additional basis (price) on which to differentiate themselves and take market share from others. Otherwise, these earnings go to the bottom line and increase profits. Either way, this is upside.

One thought on “Using Flat Legal Fees to Create a Negative Cash Conversion Cycle”